What is a Credit Score?

A credit score is a number generated by a mathematical formula that is meant to predict creditworthiness. Credit scores range from 300-850. Generally, higher credit scores may improve access to financing options and more favorable interest rates. Lower credit scores may make financing approval more difficult and may result in higher interest rates. If you have a low credit score and you do manage to get approved for credit, then your interest rate will be much higher than someone who had a good credit score and borrowed money. Over time, stronger credit profiles may help reduce borrowing costs on mortgages, auto loans, and credit cards.

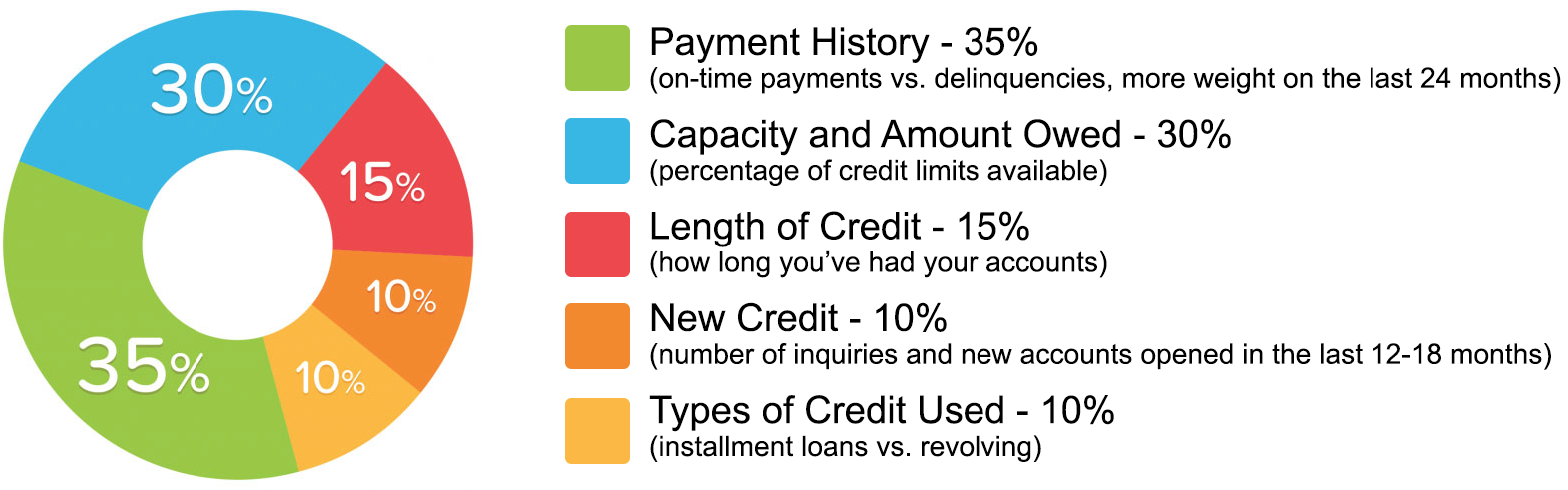

What affects your Credit Score?

Understanding Negative Items on a Credit Report

- Credit reports may contain negative items, reporting inconsistencies, outdated information, or account activity that can impact a credit profile. Understanding how payment history, credit utilization, inquiries, and account age affect credit scores is an important part of building long-term financial health. We help educate and guide clients through the credit improvement process by providing personalized support, credit education, and documentation support tailored to each individual situation.

Healthy Habits That May Strengthen Your Credit Profile

Building a stronger credit profile takes consistency and healthy financial habits over time. Making on-time payments, maintaining low credit utilization, limiting unnecessary inquiries, and keeping long-standing accounts open when appropriate may help support long-term credit health.

Regularly reviewing your credit reports can also help you better understand your credit profile and identify potential reporting inconsistencies or outdated information. Responsible credit use and consistent financial habits are key components of maintaining a strong credit profile over time.

Credit improvement is a gradual process, and every individual’s situation is unique. Our goal is to provide education, personalized guidance, and ongoing support throughout the process.

Regularly reviewing your credit reports can also help you better understand your credit profile and identify potential reporting inconsistencies or outdated information. Responsible credit use and consistent financial habits are key components of maintaining a strong credit profile over time.

Credit improvement is a gradual process, and every individual’s situation is unique. Our goal is to provide education, personalized guidance, and ongoing support throughout the process.

How long will certain items remain on my credit file?

- Late payments and delinquencies may remain on a credit report for up to seven years from the date of the original missed payment.

- Collection accounts may remain on a credit report for up to seven years from the original delinquency date that led to the account being sent to collections.

- Charge-offs may remain on a credit report for up to seven years from the original delinquency date, even if payments are later made on the account.

- Closed accounts may remain on a credit report for varying lengths of time depending on the account history and payment status. Positive closed accounts may remain longer, while delinquent closed accounts may remain for up to seven years.

- Hard credit inquiries may remain on a credit report for up to two years, although their impact on a credit profile may lessen over time.

- Bankruptcies may remain on a credit report for several years depending on the filing type and reporting guidelines.

- Certain public records and other negative reporting items may also remain on a credit report for extended periods depending on applicable reporting standards and creditor reporting practices.

- Reporting timelines and account details may vary based on individual circumstances, creditor reporting practices, and applicable credit reporting guidelines.